31 - Algorithmic stablecoins and the epic crash of LUNA/UST

We discussed last week how digital asset collateralized (DAC) stablecoins help to decouple blockchain based stable assets from the traditional financial system. Creating stability with digital assets removed the need for the third party management that fiat backed stablecoins require. Unfortunately, this autonomy comes with a cost: extreme capital inefficiency. Investors must over collateralize any stablecoin position they assume. Always looking for a way to make improvements, innovators began to think about how they could keep the autonomy that a DAC system provides without requiring over collateralization. They focused on the concept that stablecoins rely on market actors to keep them stable and how that could be used to make a capital efficient AND autonomous stablecoin.

The game theory of stablecoins

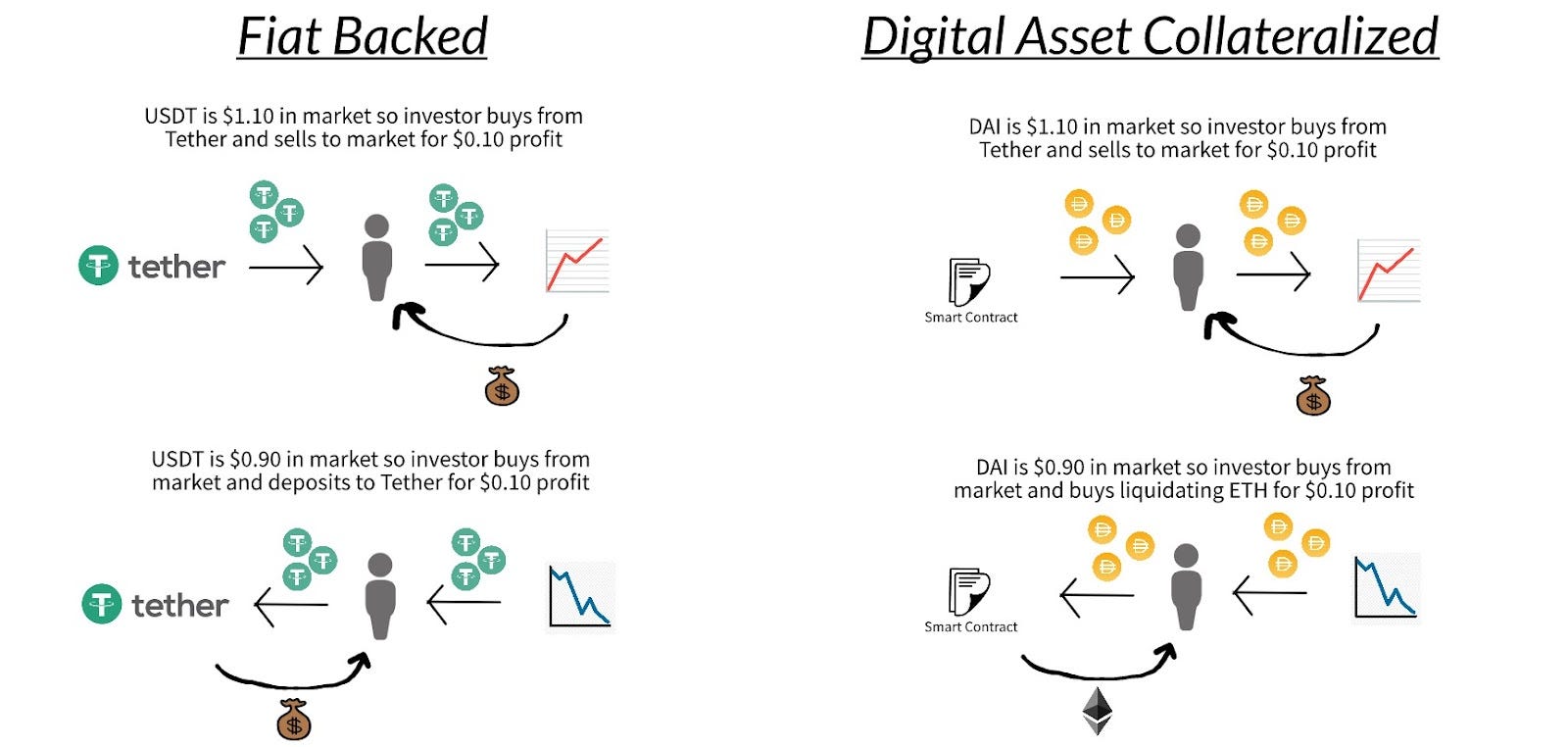

Both fiat backed and DAC stablecoins maintain their stability in large part because of a ratio of stablecoin to underlying asset. In both cases, stablecoins maintain a constant price because investors know that they can always obtain the stablecoin or that underlying asset for 1:1 ratio in a fiat backed system or 1:1+ in a DAC system. Entrepreneurs began to wonder: what if we could deploy a similar game theory but do so without requiring any fiat or digital asset collateral? Their answer was the algorithmic stablecoin.

Money profits

Although there are multiple models of algorithmic stablecoins, one of the most popular is called Seigniorage style. Seigniorage is a term used to describe the profit made by currency issuers (ie. governments) when they print bills or mint coins. The typical costs involved in currency creation include labor and raw materials. Once the currency has been issued, it has a market value; and as long as that value is more than the issuance cost, it creates a profit for the government. Governments can use that profit to finance public works or social projects. Interestingly a 2016 study found that the US penny costs about 1.5 cents to make–obviously not the most profitable endeavor the US government has engaged in.

Coming back to the world of digital assets, Seigniorage style stablecoins rely on the concept of currency inputs to create and help maintain stable assets. Many of the input costs of traditional currency creations are used to prevent the forgery of money and the devaluation of the dollar through increased supply. In the digital world, currencies are not made from metal and other inputs but rather from bits and bytes which are basically free. The need for some kind of input necessitated that Seigniorage style stablecoins rely on a two token system to work. One token will be the stablecoin and the other will be the input required to create that stablecoin. The best way to explain this is through the example of the now infamous LUNA/UST system.

LUNA and UST

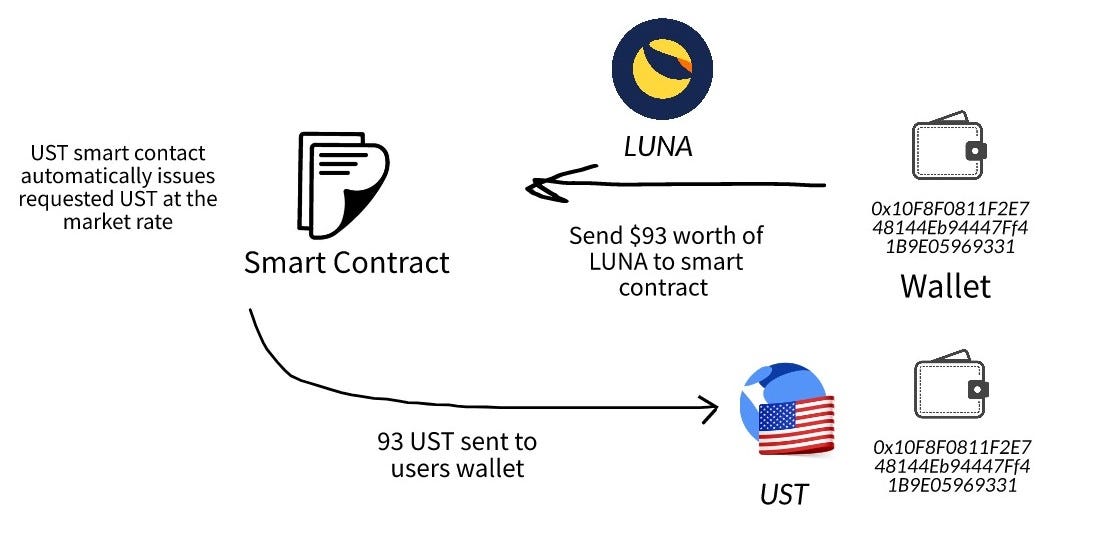

UST, like USDT and DAI, was designed to be stable against the US dollar and LUNA was created to be its input. The system was designed to ensure UST maintained its $1 peg through a mint and burn smart contract. Investors could buy LUNA and redeem it for UST on a 1 : market value ratio. If LUNA has a market price of $100, then you could burn (destroy) it and receive 100 UST. The system relies heavily on game theory to operate.

Whenever UST moves above a dollar to say $1.05, investors could redeem LUNA for UST and then sell that UST on the open market. The issuance of more UST would expand the UST supply and over time reduce the market value. The same process could happen in reverse. If UST de-pegs on the down side to $0.95 then investors could buy up the cheap UST and redeem it for $1 worth of LUNA. The key difference between this model and a DAC stablecoin is that there is never a point at which the UST smart contract will try to liquidate LUNA to control the supply of UST similar to how the DAI smart contract will liquidate ETH collateral. In theory this sounds brilliant and creates the capital efficient stablecoin the industry is looking for. It also mimics in some high level ways how the successful traditional fiat issued currency system works today. Unfortunately it is flawed.

The big issue with this model is that it relies on market actors acting “rationally” (as defined by the makers of the LUNA system) and independently, two things that rarely happen simultaneously especially when markets start to decline. The market price of LUNA theoretically is driven by how many people want UST and the total supply of LUNA. As long as demand for UST is high, then there will also be demand for LUNA. The supply of LUNA will decrease each time an investor burns some to obtain UST which should then increase the price of LUNA. Core to the model is the belief that there will be demand for UST but is there really?

The crash

The reason people want the US dollar is because it is the most trusted currency in the world and is still the most widely held reserve currency by foreign central banks. Most foreign debt is denominated in US dollars, and significant amounts of remittances around the world are settled in US dollars. There is huge demand for dollars which is in part why the US Fed feels that it can be somewhat reckless with the printing of dollars at least in the short term. UST is not the US dollar, and there is not this much demand for it.

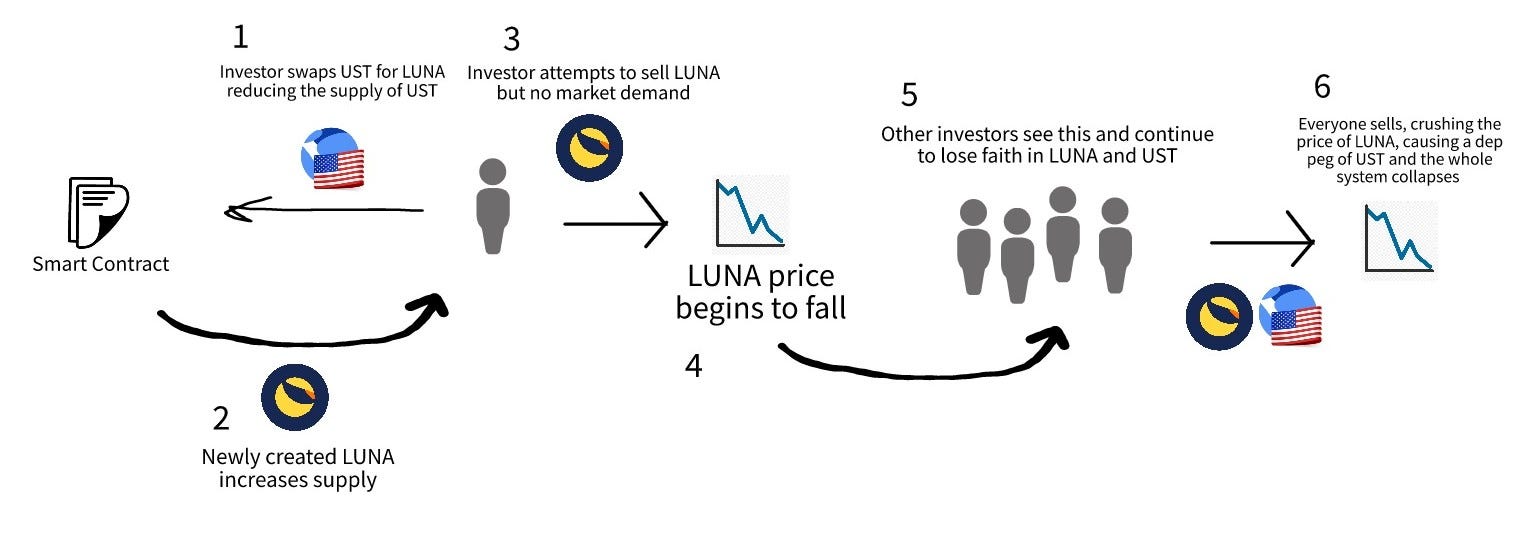

On May 7, 2022 the fundamental principles of this model were tested and failed. Sparing you the detail, the broader crypto market’s decline caused investors to exit their UST positions, selling their UST for other assets. The lack of demand for UST caused the price of LUNA to decline after it had already dropped thanks to the broader digital asset market sell off. LUNA’s decline made investors uneasy about the entire project and how effective it would be at maintaining UST’s $1 peg. In what could be called a self fulfilling prophecy, investors who were spooked continued to sell out of both UST and LUNA which caused the UST peg to decouple.

We discussed earlier that when this happens, “rational” investors should come in, buy UST on the open market, and then swap it for LUNA on a $1 : Market ratio. That plan only works if investors want LUNA. LUNA’s value being tied to the whole UST ecosystem meant that investors were not interested in owning the asset. Investors were acting in unplanned coordination to sell off both UST and LUNA, crashing the price of both. The digital asset industry fondly referred to this event as a “death spiral.” Unlike the US dollar, when push came to shove, there was no demand for UST. The creators of the LUNA ecosystem had tried to create demand by funding projects that would use UST as their stablecoin; but in a down digital asset market, there were no longer users wanting to use those projects.

The takeaways

Algorithmic stablecoins are the latest stablecoin iteration and are an attempt to be more capital efficient than fiat backed or digital asset collateralized stablecoins. They rely on the theory of the rational investor to maintain stability; but as we have seen with UST and LUNA, there is no guarantee that theory withstands reality. There are other algorithmic stablecoin models that might work; but for now, the digital asset market is wary of them. Regardless, stablecoins in whatever form they take have value in this ecosystem and will continue to garner attention and curiosity from anyone working or investing in the space. They provide the incredibly important service of blockchain based stability and will most certainly play a role in the future of the industry.