30 - Digital asset collateralized stablecoins

Fiat backed stablecoins are the stable juggernaut of the digital asset industry. We spoke last time about what these assets are, as well as their advantages and disadvantages. One major disadvantage was that they required an organization to manage a bank account and control issuance of the stablecoin. For the top two stable coins, USDT and USDC, those organizations are Tether and Circle respectively. For an industry founded in self sovereign wealth, an asset that can be controlled by a single entity was unacceptable. Entrepreneurs began to explore how to design a stablecoin that would not require third party management. Where they landed was a digital asset known as “collateralized stablecoins.”

Digital asset collateralized stablecoins

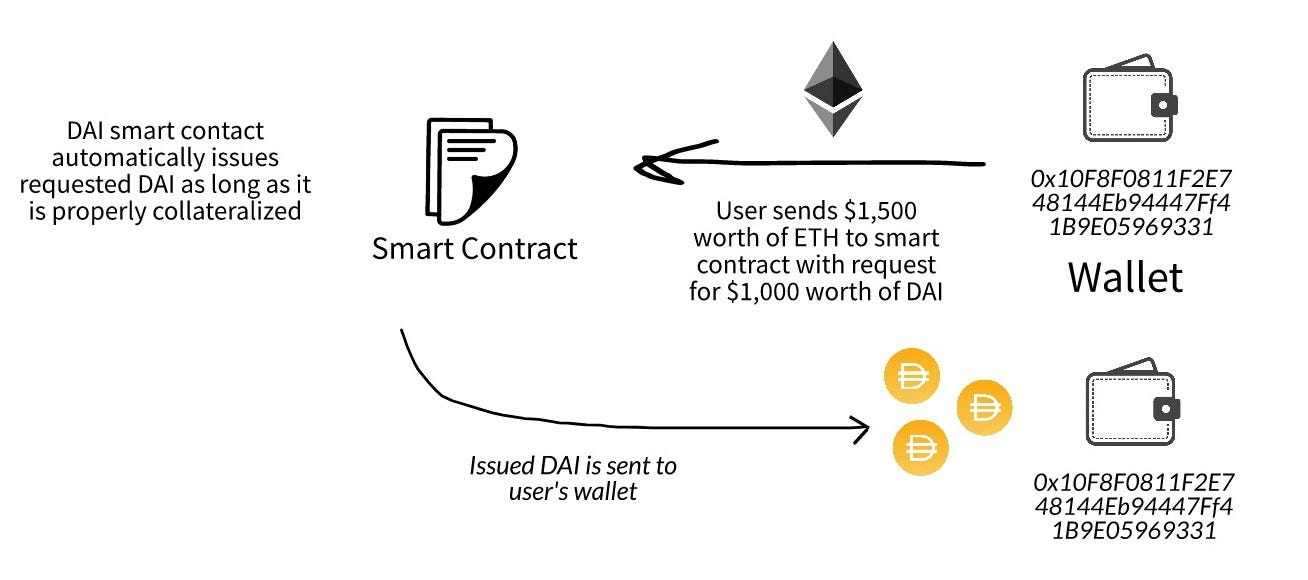

The concept of a digital asset collateralized (DAC) stablecoin is simple. Instead of depositing dollars into a bank account after which a management company issues the depositor the correct amount of stablecoins, investors would deposit digital assets such as ETH into a smart contract that would automatically do the issuance. The smart contract-based system would create a completely autonomous and blockchain based form of stable asset. It would eliminate the need for a middle man to bridge the gap between a traditional finance bank account and the world of blockchains. The system would also reduce the risk that assets would be frozen or confiscated.

Some readers might be wondering: doesn’t this bring us full circle? How do you create a stable coin with an asset like ETH that is extremely volatile? Wasn’t the whole point of the stablecoin to move away from the traditionally volatile assets? These are good questions, and the answer lies in how the digital asset collateralized stablecoin (DACS) is designed. Many designs have been tried, but the first successful version of a DACS was Maker DAO and its stable coin DAI.

Maker and DAI

DAI is the best known DAC stablecoin and is the fourth largest stablecoin by market capitalization after the fiat backed coins USDT, USDC, and BUSD. The Maker foundation launched DAI on the Ethereum blockchain in 2017, and their model was quickly adopted as the gold standard for DACS. When we say launched here what we mean is to create the smart contracts that are the foundation for the whole DAI system. Smart contracts can work autonomously, but someone or organization needs to create them.

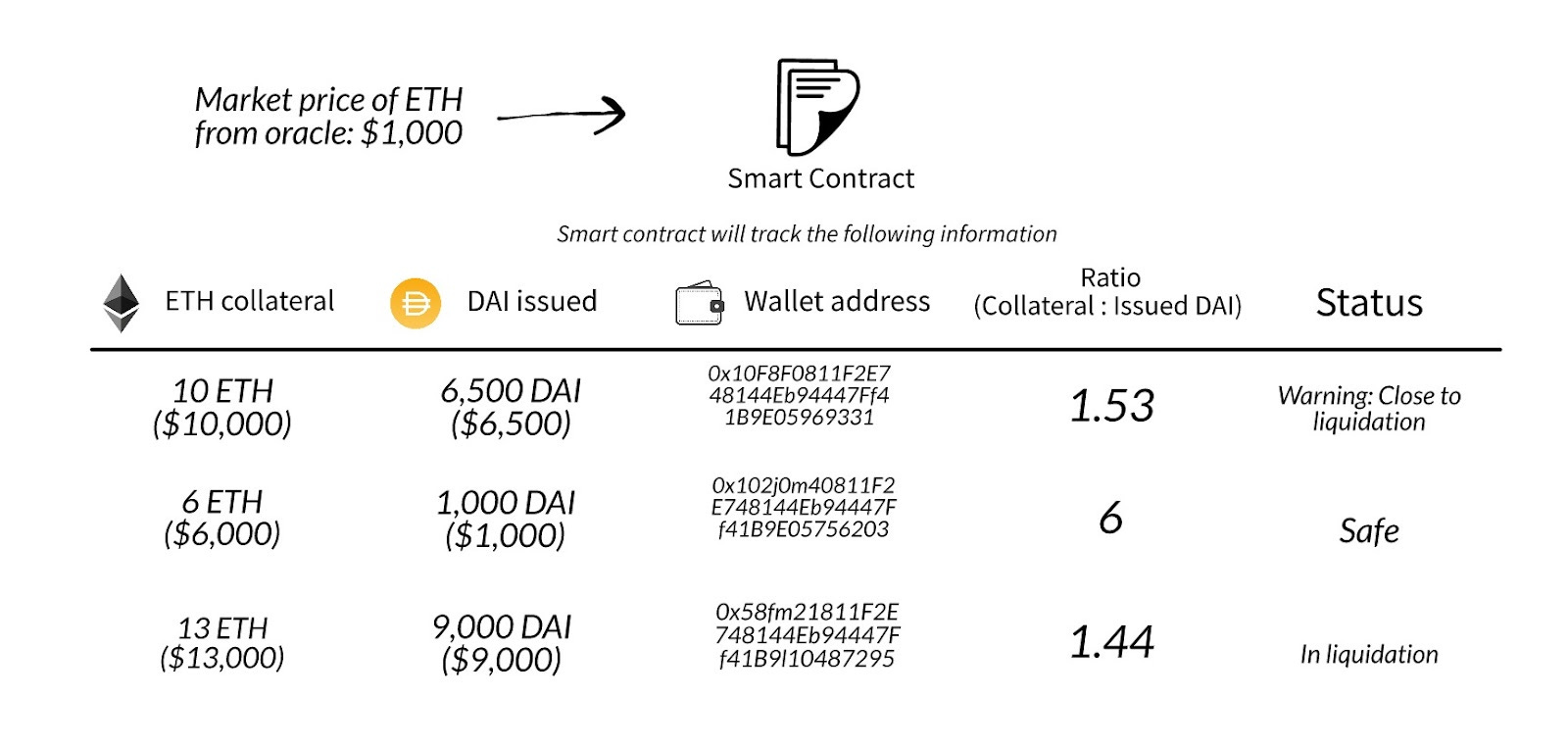

The key to the DAI design’s success rests on the concept of over collateralization and liquidation points. If an investor wanted to obtain DAI, they needed to send a digital asset (at launch you could only send ETH but now the system supports other digital assets) to the Maker’s smart contract which would then issue DAI based on the market price of the ETH the investor sent. The catch is that the Maker contract required the investor to send ETH worth more than the amount of DAI they wanted to receive. If someone wanted $10k worth of DAI, they needed to deposit at least $15k worth of ETH in order to account for the volatility. More specifically, the requirement to over collateralize the DAI issued created a buffer so that if the price of ETH collateral dropped, it wouldn’t impact the stability of DAI. It is however possible for the collateral to lose so much value so quickly that it would disrupt DAI’s stable $1 price. Maker uses a liquidation ratio to help stabilize DAI’s price if this situation were to ever occur.

The liquidation ratio is the minimum amount of overcollateralization required by an investor in order to obtain DAI. If the market value of the collateral drops below this ratio then that collateral will be sold for DAI. If the liquidation ratio is 1.5, then anyone wanting to create DAI will need to deposit at least 1.5x the amount of DAI they are creating. If your collateral's market value dropped below that 1.5 collateral to 1 DAI ratio to say 1.4 collateral to 1 DAI, the collateral would be auctioned off by the Maker smart contract at a discount for DAI. The asset discount incentivises people to buy that collateral and requiring that DAI be the medium of exchange, would reduce the total DAI in circulation and ensure the total DAI supply was at least 1.5x the total market cap of the collateral in the Maker smart contract. In summary, the whole crypto collateralized system is based on overcollateralization, a liquidation ratio, and economic incentives to purchase bad collateral at a discount. You can look more into that here.

When the system fails

History has shown that even if you do create a sound system like Makers, there is still the potential for issues. Back in 2020, the Maker system experienced market dynamics that put its system to the test. COVID-19 caused a societal and subsequently a market meltdown which resulted in extreme price fluctuations. The volatility was most extreme in the crypto markets from March 10-20th. The extreme price movements resulted in investors rushing to sell their digital assets. In order to sell their assets, including those on the Ethereum network that investors needed to transfer them from their personal wallets to an exchange. The mass movement of assets caused extreme congestion on the Ethereum network. At the same time, the volatility was making it hard for exchanges to provide accurate pricing data. Keeping up was close to impossible.

The Maker system uses price feeds to inform the system about how much the collateral backing DAI is worth. These feeds are called oracles which are managed by third parties. Maker uses multiple oracles to ensure that the price it is getting from any one oracle isn’t off from the broader market. In normal times, the system works well, with one oracle providing checks and balances against the others; but in March none of the oracles were able to keep up with the ever changing market. The combination of a slow network and inability to keep an accurate price resulted in faulty collateral auctions at Maker.

Fire sale

When the Maker system receives pricing data that shows an investor’s collateral is close to hitting the liquidation point, the system tells the investor they need to add more collateral to prevent their assets from being sold. If the investor does not provide more collateral, then the system liquidates the collateral it does have. The March 2020 price volatility caused the Maker feeds to go haywire, resulting in auctions where ETH collateral was sold off to purchasers for prices well below the market rate, all the way down to $0. Even in the wild times of 2020, the actual market prices of ETH never went below $90. At the same time the network congestion was causing some investors' who were attempting to add more collateral to their DAI position to have their transactions rejected and their collateral to be unfairly liquidated.

The microcosm not only shook faith in the Maker system, but also caused the price of DAI to depeg. Interestingly the depeg did not push the price of DAI below a dollar but rather made it rise above a dollar to hit a high of $1.12. Investors knew they could get cheap ETH from the Maker auctions but did not want to obtain DAI by posting collateral in case it too was liquidated. They were instead buying DAI on the open market, causing the demand to spike and subsequently the price. Since then the price of DAI has stabilized, and it has continued its reign as the most used DAC stablecoin on the market.

The takeaway

In an attempt to move away from fiat backed stable coins, the digital asset industry created the digital asset backed (DAC) stablecoin. These assets rely on an over collateralized system where the assets backing them are worth more than the value they’re creating. DAI is the most popular and widely used DAC stablecoin and has been a staple of the digital asset space since its launch in 2017. As always, the digital asset industry seeks perfection; and although DACs have been successful, many people in the industry want an asset that is as capital efficient as a fiat backed stable coin without the need for a bank. Moving beyond DACs, audacious individuals have begun to attempt what many believe to be impossible: Creating an uncollateralized stablecoin that relies on market dynamics to maintain its stability.