Opinions expressed are solely my own. Shout out to my friend and colleague John Schneider and my parents for some great edits.

Bernard

Since the early 1900’s, Charles Ponzi and his scheme have been the go to analogy for financial fraud. Charles had been arrested in 1920 for offering investors 50% returns in 45 days and 100% returns in 90 days. It turns out those returns were generated by Ponzi paying out earlier investors with later investor’s money. In modern times many people believed that technology, information sharing, and investor sophistication had advanced to such a degree that the public could avoid these forms of deception. That was until December 10, 2008 when Bernard L. Madoff revealed to his sons that he was operating the largest Ponzi scheme ever to be uncovered.

Bernard, who went by “Bernie”, cut his teeth in financial markets in 1960 after founding Bernard L. Madoff securities (BMS). BMS was a broker-dealer firm that initially specialized in penny stocks and less liquid over the counter (OTC) securities known as the “pink sheets”. Over time, BMS proved to be an innovator in the financial services industry, helping to create technology that made price discovery in the opaque OTC market more transparent. That technology eventually became the National Association of Securities Dealers Automated Quotations Stock Market (NASDAQ). By all metrics, BMS and Bernie were a huge success. At one point, BMS was the largest market maker on the NASDAQ; and in 2008, it was the sixth largest market maker in S&P 500 stocks. Bernie served as Chairman of both the NASDAQ and National Association of Securities Dealers (NASD), a financial industry self-regulatory body, for multiple years.

In addition to his successful market making business, Bernie also operated a private, unregistered wealth management business on the side. He was extremely secretive about this business, which included keeping its office on a separate floor from his legitimate operation and excluding any of his family members from participating in its operation. There is debate as to when Bernie began committing fraud. He claims it was an effort to cover up losses from the 1989 crash; but there is evidence that it began much earlier. Just like Charles Ponzi before him, the scheme was simple: collect investors’ money and pay out unheard of returns. These returns were not the 100% in 90 day returns Ponzi promised, but rather steady, above market returns that could be counted on regardless of what the market did. Such consistent returns were attractive to a more conservative crowd.

On March 12, 2009, when Bernie pled guilty to 11 federal felonies, the total amount of missing investor money was $65 billion. Many people have asked how a crime of this magnitude could have gone undetected for so long, and the answer is that it didn’t. The Madoff scheme was reported to the SEC on three separate occasions in the early 2000’s, but was never fully investigated. In fact, there was one instance in which Bernie blatantly lied to the SEC officials about total investor holdings he claimed were at the Depository Trust and Clearing Corporation (DTC). All the agent had to do was call the DTC; and he would have learned that Bernie’s advisory business didn’t even have enough money to buy a cup of coffee, let alone the tens of billions he had claimed.

Kenneth

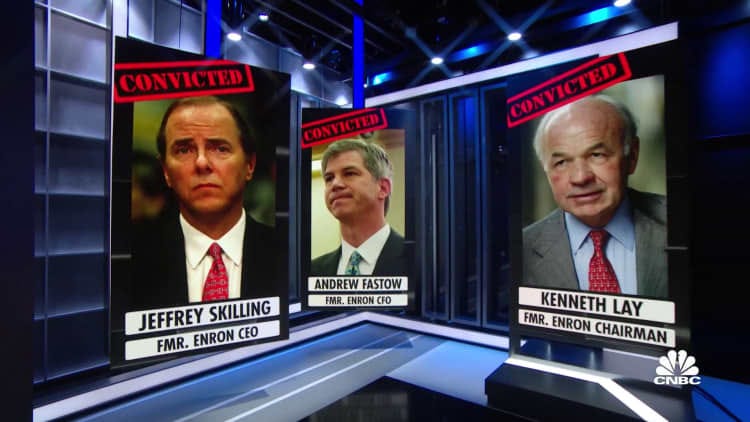

In late 2000, when Bernie was being questioned by SEC officers, Kenneth Lay, the CEO of the United States sixth largest company, Enron, was stepping down from his position. It was December, and the past year had been a great one for the company with its stock price hitting an all time high of $90. It was the third consecutive year that Ken was going to be the highest paid CEO in the United States; so it was a bit odd that a man seeming to be at the top of his game running one of America’s darling companies would want to step away. What would soon come out was that the company and man whom many admired were involved in deception of biblical proportions.

Enron was formed in 1985 after a merger between Houston Natural Gas and InterNorth. The new company originally operated natural gas pipelines that spanned approximately 37,000 square miles. Like many large companies did in the late 80’s and 90’s, Enron began to move outside of its core business and into that of financial markets. In 1989, the company entered the natural gas commodities trading business. At this time, Enron also made two key hires: Jeffery Skilling and Andrew Fastow. Over the next eight years, Skilling and Fastow would gain significant power within Enron; and by 1998, Skilling was President and Chief Operating Officer, and Fastow had just been appointed Chief financial Officer.

Starting as early as 1993, Fastow with the approval of Kenneth Lay had begun to play games with Enron’s financials. Being an innovative company (it was named “Most innovative company in America” by Fortune magazine every year between 1996 and 2001), Enron had been taking massive risks. In order to hide enormous losses from its derivatives trading and industrial investments, Fastow began to offload these losses to special purpose vehicles (SPV’s).

These SPVs were formed by sponsors outside of Enron but coordinated by Fastow. The purpose of these companies was to essentially “buy risk” from Enron either in the form of acquiring Enron’s debt or potentially impaired assets and trading positions. The result was an accounting sleight of hand. Thus Enron had a dumping ground for underperforming investments allowing them to offload the negative impact to their financials. To outside parties, it appeared Enron had found a buyer for assets when in reality Enron was essentially selling losses to their own subsidiaries.

In December of 2000, Ken realized the extent of the accounting malpractice and decided to step away while he still could. The board appointed Jeff Skilling as CEO, a role he resigned from shortly thereafter, forcing Ken to return to Enron. Over the next year, Enron was forced to make major accounting corrections, including: restate earnings for 1997 through 2001, reduce those earnings by over $600 million, increase liabilities to $634 million, and reduce stockholder equity by $1.2 billion.

On November 28, 2001, after a failed merger with Dynger, Enron filed for Chapter 11 bankruptcy, obliterating what had once been a $60 billion company. During the proceeding John Jay Ray III was appointed as Chairman to help the company navigate bankruptcy. Skilling and Fastow pled guilty to multiple charges and served several years in jail. Lay was found guilty of securities and wire fraud, but died prior to his sentencing. The international accounting firm Arthur Anderson, which was responsible for auditing Enron’s financials, eventually collapsed under the avalanche of lawsuits filed against it.

Samuel

At the time of the previous blog post there was still much to learn about the collapse of FTX. Since then, much has transpired with one of the more notable events being the appointment of John Jay Ray III to oversee the dissolution of FTX. Yes, this is the same John Jay Ray III that oversaw the dismantling of Enron, as he has been appointed as CEO of the defunct crypto empire. Ray has a long career overseeing bankruptcy proceedings, starting with Fruit of the Loom in 1999. After Enron, Ray worked on the bankruptcy proceedings of Nortel, Residential Capital, and Overseas Shipholdings. One of his first acts as CEO of FTX was to file bankruptcy petitions. In these submissions, Jay outlines the status of the FTX group and the changes he is making to help shore up the remaining company assets.

The section that stood out to most people was found on the second page of the filing. Jay states:

Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information as occurred here. From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented.

This comes from a man who was charged with investigating and unwinding countless other companies, including what previously had been characterized as the most epic financial deception in history.

Another section that received significant press was the footnote of page 6 where Jay outlines the details of a loan issued to struggling crypto lender Blockfi. What makes this footnote stand out is the loan was made of $250 million worth of FTX’s FTT token. Providing the loan in FTT token meant that there was a high likelihood that the solvency of Blockfi itself was closely tied not just to FTX US, but also to the price of the FTT token. At the time of Blockfi’s loan, the total market cap of FTT was around $4.01B. The loan of $250 million would have represented 6.25% of all FTT token. In a small market with limited volume, 6.25% of total supply would have been impossible to sell without greatly impacting the price of FTT. Being unable to sell significant amounts of the token would have meant Blockfi most likely still holds much of the loan in FTT that has declined over 90% since the loan was issued.

Along with these two notable sections, the document is full of other interesting observations made by Jay, including:

Many of the companies in the FTX group never had board meetings or in some cases a board.

FTX had extremely poor cash management procedures, including not having a full and accurate list of all entity bank accounts.

Jay has substantial concerns about the legitimacy of the audits conducted on certain company financials.

FTX’s employee management was in disarray, resulting in the inability to create a complete list of employees. The total number of both contractors and full time employees is unknown.

Property was purchased under the names of top company officials and SBF family members using company funds.

Clearly, Jay and his team have just started to uncover all that was wrong with FTX.

Judging business failure

The current state of the crypto industry is that everyone is attempting to make sense of the debacle and more critically find someone to blame for the mess. The company is being compared to the likes of Lehman Brothers. The name of former CEO Sam Bankman Fried (SBF) is being used in the same sentence as Ponzi, Lay, and Madoff. The comparison between these institutions and their leaders is not unfair, but in many cases, is misplaced. In order to understand why, let’s talk about entrepreneurship.

Starting a business is risky but has the potential to be extremely rewarding. The risky part of the endeavor is that the business can fail, and that’s the aspect we are going to focus on now. One of the reasons the United States has been home to some of the most innovative companies in the world is because we have made it okay to fail. Entrepreneurs are free to experiment knowing that there is little downside if they don’t succeed. Societies need individuals willing to take the risk of starting a business, because it brings innovation and job creation, and stimulates competition.

The risk taking and failure acceptance mentality has resulted in massive returns for the United States, but there are rules. It is okay to fail due to changes in market conditions or personal circumstances as long as the actions taken by the entrepreneur align with what they communicated to their investors and customers. A successful business’ failing is one led by honest leadership.

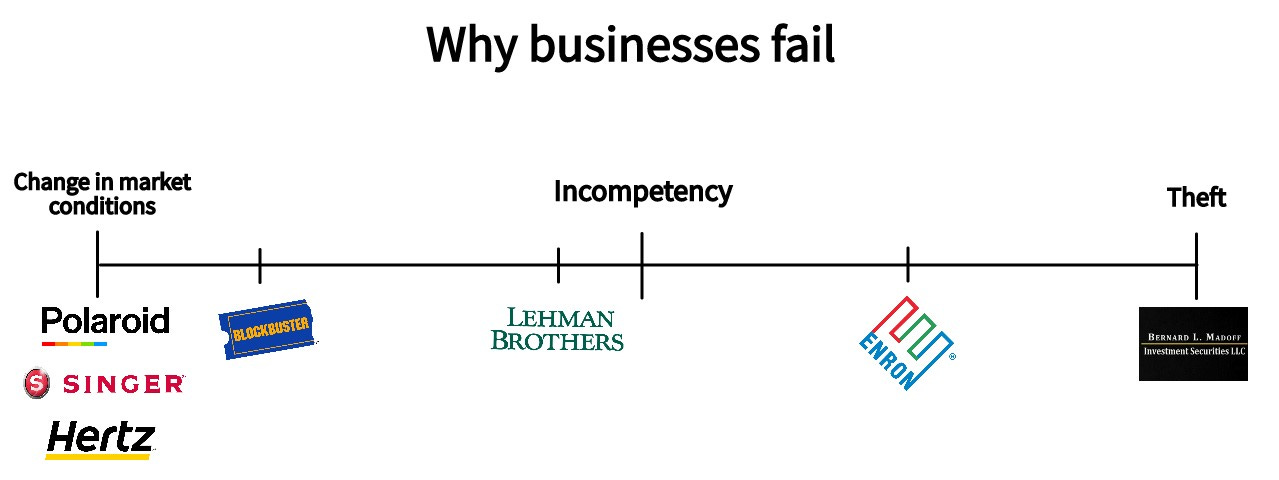

You can think of corporate failure on a spectrum with outright “theft” on the right, “change in market conditions” on the left and “incompetence” in the middle.

On the left we have “changes in market conditions” and companies like Polaroid, Singer, and Hertz. All of these businesses suffered after a change in market conditions: Polaroid lost customers to digital cameras; Singer fell when Americans stopped making their own clothing; and Hertz was a casualty of COVID when travel was non-existent. Each one had a legitimate product, and their leadership did as much as possible to keep the companies afloat.

In the middle we have “incompetency” which focuses on businesses that failed thanks to the poor business practices of their leaders. Lehman Brother is the prime example of incompetent business leaders. Richard Fuld, the CEO at the time of its collapse, was notorious for an authoritarian style of leadership and willingness to take extreme amounts of risk. Lehman failed because it had taken large bets on mortgage loans that would default at an incredible rate. Its demise played a large part in the financial pain that marked the 2008 recession; but its failure had more to do with the risk it assumed and changes in market conditions than it did any fraudulent acts of Fuld and his deputies.

On the right we have “theft” where a business fails because it is a charade. Enron belongs somewhere in between the middle and the extreme right of our spectrum. Enron’s leadership lied and actively deceived regulators, auditors, and investors, but there was no actual theft. It could be argued that their lies allowed them to unfairly receive compensation that they shouldn’t have, but there was no direct pocketing of customer or business money. Bernie Madoff’s investment advisory business was, on the other hand, outright theft. He used his strong reputation from his legitimate broker dealer business to put investors at ease, and in so doing, steal their funds.

Placing FTX

Placing FTX on this spectrum is going to be hard. Every US citizen deserves a right to fair trial, so making any claims about FTX and SBF prior to that occurring would be premature. However, there are some facts about the reasons for FTX’s bankruptcy that give us clues as to where on our spectrum the company could fall.

First, SBF and the CEO of Alameda Research, Caroline Ellison, have admitted to using FTX customer funds to shore up the balance sheet of Alameda. In some businesses, this would not be illegal, except that SBF has historically been relentless about supporting customers, assuring outside parties that customer funds held on FTX are safe, and that the exchange does not engage in rehypothecation. Second, it was revealed in the court filing documents that Alameda Research lent $4.2 billion to parties related to the company, including a $1 billion personal loan to SBF. Third, Reuters has reported that SBF, his parents, and FTX senior staff have used as much as $300 million dollars for personal property purchases.

As of today it appears that FTX was a legitimate business that was run by individuals with questionable morals and it was not a Ponzi scheme. CEO’s like Kenneth Lay don’t go to jail because their businesses begin to fail; they go to jail because they lie about their struggles, actively try to hide them, and sell their stock based on that information. The problem with the actions outlined above is that FTX leadership lied about those actions publicly to customers and most likely privately to investors. The lies about a business’s success allow leaders like Theranos’ Elizabeth Holmes to raise money and those lies are what end up biting them in the butt. Everyone has the right to raise money, start a business, and fail. What they don’t have a right to do is lie about their results or intended actions. My guess is that FTX is going to land somewhere in between an Enron- and - Madoff-type fiasco.

Another interesting dynamic playing out right now is between the angered digital asset community and the media. There are many news outlets reporting on FTX with an assumption of foul play; but there are also many outlets that still aren’t letting go of the heroic investor image SBF portrayed prior to the exchange’s collapse. A prime example is the New York Times (NYT) DealBook summit where SBF is still on the agenda to be a speaker. The Wall Street Journal (WSJ) is also being excoriated for publishing what many perceive as FTX puff pieces. Maybe these publications believe in the need to protect the entrepreneurial spirit or maybe they are being opportunistic. After outcry the WSJ changed the title of the article from “When Sam Bankman-Fried’s crypto empire went down in flames, so did his plans to save the world” to “Sam Bankman-Fried Said He Would Give Away Billions. Broken Promises Are All That’s Left.”

While everyone deserves their day in a court of law, in the court of public opinion, a verdict has already been rendered. SBF should be recorded in the annals of history next to Bernie Madoff not Richard Fuld.