25 - Decentralized finance

25 - Decentralized finance

4 feet 8-½ inches… that is the standard “gauge” of a railroad track or the distance between the inside vertical surface of a rail. It is an odd number but traces its origins to horse drawn chariots in Rome. Despite its heritage, railroad tracks have not always been standardized. In the late 1800’s, there was a long battle around the standardization of a rail width. Northeastern railways used the standard; Pennsylvania used 4 feet 9 inches; Southern railroads 5 feet; and Canadian railroads used 5 feet 6 inches.

The different sizes caused enormous problems. When traveling long distances, passengers often had to transfer across multiple train lines in order to reach their final destination. The lack of standards caused a logistical nightmare but eventually was resolved in the early 1900’s with the introduction of a 4 foot 8-½ inch standard. Establishing a standard helped connect railroads, allowing train cars and train stations to be used interchangeably by railroads. The move to a standard railroad width accelerated railway development and helped to increase rail travel's attractiveness to passengers.

Similar to the impact a standard rail width had on railroads, token standards like the ERCs on Ethereum have helped to create a massive ecosystem of blockchain networks. In The Promise of Smart Contracts we learned that smart contracts are virtual agreements. The example we used was placing a bet. You can code a smart contract to help place a bet on the Super Bowl. You create a contract that will pay out assets based on a certain outcome . Token standards help smart contracts operate more efficiently. Establishing the ERC20, ERC721, and numerous other standards, has allowed smart contracts to be created to service a specific standard rather than a specific project. This simple fact has led to the rise of one of the most exciting industries being built on top of blockchain networks: Decentralized finance.

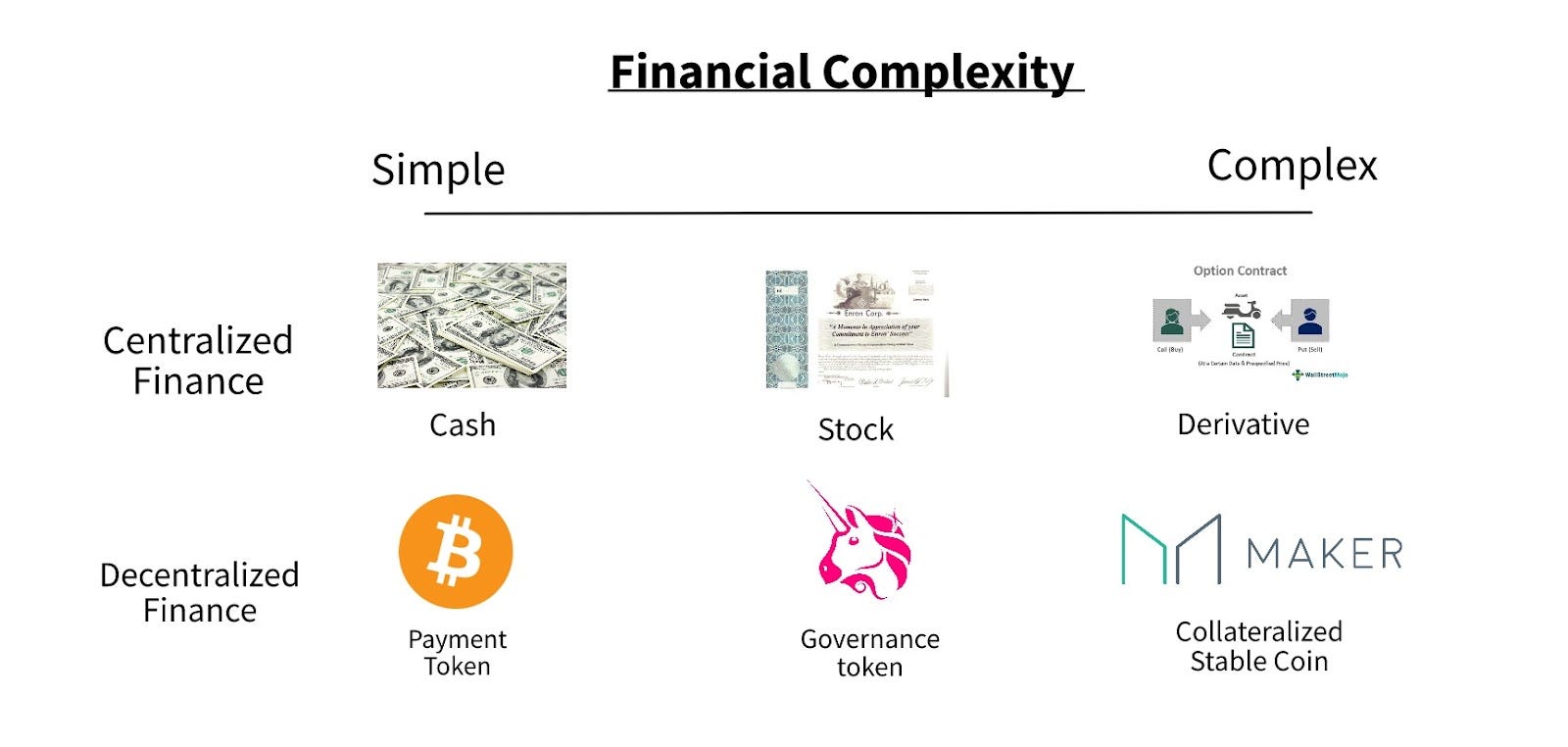

Centralized and decentralized finance

Before unpacking decentralized finance, let's quickly chat about centralized or traditional finance. When we say “traditional finance,” we are talking about the system of banks, payment processors, investment firms, and organizations that facilitate the transaction of money between parties. The common vernacular describing these institutions is “third party intermediaries.” Historically, their role was to help ensure trust in a transaction. Serving this role allowed people who relied on them to transact with strangers and not need to carry around large sums of cash.

Bitcoin was the first digital asset created as an alternative to a cash payment; but other financial services investing, lending, and borrowing are a bit more complicated. All of these activities require more information than simply the sender and receiver. They require discretion (which is usually the job of the third party) such as understanding the credit- worthiness of a borrower. Smart contracts can be used to replicate this discretion by replicating the analysis process most of these third parties go through.

Decentralized finance, often known as “DeFi”, can be defined as the ecosystem of smart contracts that allow individuals to conduct complex financial transactions with other actors without the need for a bank or other third party to serve as an intermediary. If we were to create a spectrum of complex financial transactions, sending and receiving money would be on one end and taking out a loan against collateral and using that loan to buy options would be on the other. Bitcoin and blockchains in general give us a way to send and receive money outside of traditional finance, but we need smart contracts to help us move from left to right. Smart contracts help us to bridge the gap between a present moment transaction and a point in time transaction. Through smart contract code you can create event dependent value transfer and other more advanced financial transactions. Let's explore three current use cases for how smart contracts are being used to replicate traditional financial services.

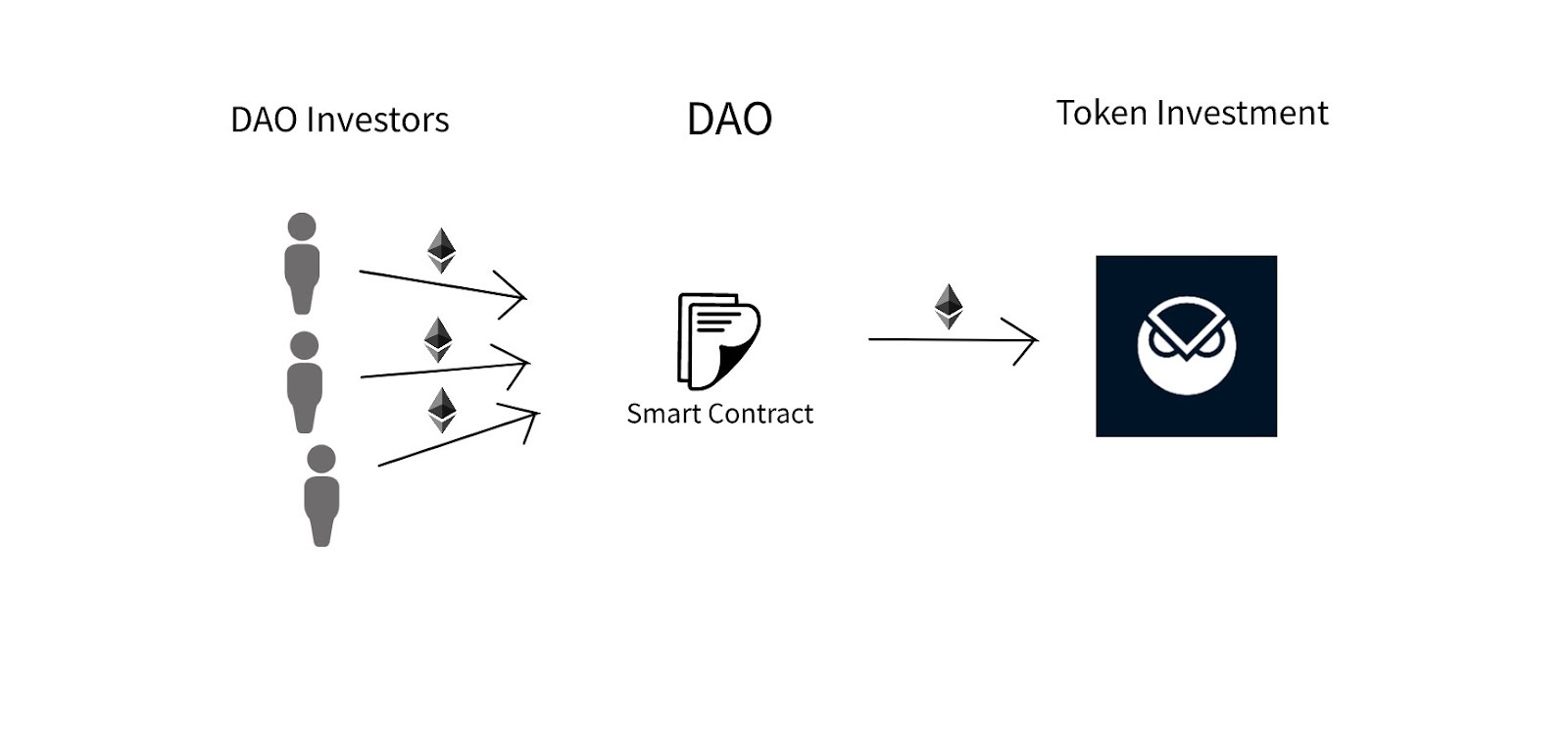

DAO’s

The first real example of DeFi replicating traditional finance is to mimic asset management through something called a DAO. “DAO” is an acronym for “decentralized autonomous organization.” DAO’s are smart contract-based investment vehicles. Particpants pool their money in a smart contract and in return receive a DAO token. DAO tokens represent a vote in how the DAO invests the committed funds. If another token project is a token, then the DAO could choose to invest in that project by sending their funds to the new token’s smart contract. In this way, DAO’s are able to make investments.

The difference between a DAO and something like an LLC or corporation is that the DAO is organized on a blockchain and 100% publicly auditable. What this means is that the funds sent to the DAO can be seen by everyone at all times. Remember that blockchain records are public and transparent, so anyone who’s a part of the DAO can see exactly what the value of their investment is and where their investment is going. It also means that funds are allocated based on a vote rather than by a single person such as an asset manager, thus giving the DAO members more of a voice in how funds are allocated. Replacing an asset manager with a smart contract and voting process also helps to reduce cost. The first well known DAO was created in 2016 and called “The DAO.” The story of The DAO is an important part of blockchain history and a source of controversy amongst the Ethereum and broader blockchain community.

Market Making

The second innovation in DeFi was to replicate a stock market. In traditional finance, to buy or sell a stock you needed to do so on an exchange like the NASDAQ or NYSE. Buying and selling stock is functionally a very simple transaction, but finding someone to buy and sell with is the hard part. Traditional exchanges provide a place where anyone can go to find others with whom to transact . Interestingly, no individual can go directly to NASDAQ or NYSE to make an exchange. Instead you must get an account with a brokerage that then places trades on your behalf.

Smart contracts can be used so that anyone who wants to sell or buy an asset only has to send that asset or the payment to a smart contract and that smart contract will match the buy orders with the sell orders. One of the earliest examples of this kind of market was Radar Relay. Unfortunately this structure, called order book matching, does not solve the problem of there not always being a buyer or seller or vice versa. DeFi has evolved past the original simple order matching structure and now mostly uses something called “liquidity pools.” We will dive deeper into how trading in DeFi works today in next week’s post.

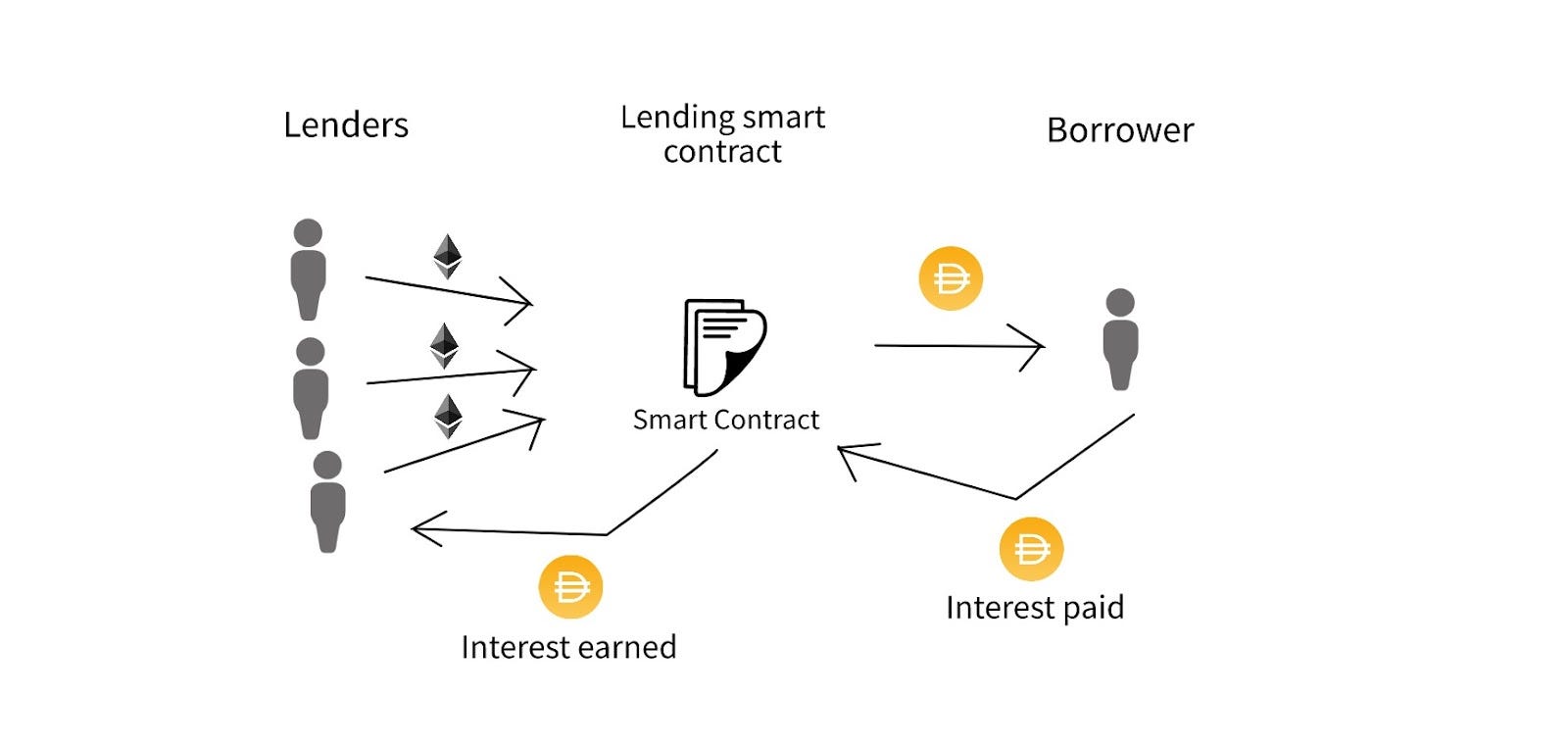

Lending

Finally, DeFi has come up with some creative ways for digital asset users to access money to borrow. In the traditional finance system, people deposit money in a bank account;the bank takes those deposits and lends them out to other people looking to borrow. If you wanted to borrow money, you would go to a bank and apply.

The bank assesses your application based on criteria known as the four “C’s”: capacity, capital, collateral, and credit. Capacity is your ability to make payment usually determined based on income; capital is how much money you have at the bank; collateral is anything of value outside of liquid cash you own, such as a house that could be used to pay back the loan; and lastly, credit is a person's credit score calculated based on your track record of managing past loans. As you could probably guess, getting a loan is not easy.

DeFi abstracts away the bank and three of the four “C’s.” Instead of the system outlined above, smart contracts can be created that will lend to anyone with enough collateral. In a collateral-based lending system, anyone can send x number of a digital asset to a smart contract and receive a loan from that contract. One of the most well known lending projects is Maker.

Maker allows anyone to deposit ETH and some other select digital assets into their smart contract and in return receive DAI, a different kind of currency known as a stable coin. The catch is that the value of the digital asset you deposit must be below the value of the loan. If I deposit $10,000 worth of ETH, then I can only get a maximum loan of $4,000. I can do anything that I want with that loan; and if I want my $10,000 worth of ETH back, all I have to do is deposit $4,000 worth of DAI back into the contract. There of course are nuances to this system that I will be discussing in a future post.

Take away

The smart contracts that serve as the foundation for DeFi present an enormous opportunity. What we have discussed today only scratches the surface of DeFi’s potential and the intricacies of the space. In the coming weeks we will dive into all things DeFi and get a better understanding of why the ecosystem is so appealing to so many.