The fascinating part about the blockchain industry is that it was created organically by a small group of people online. Developers communicated by email and group chat to create the first Blockchain, the Bitcoin Blockchain. The very nature of this nascent technology dictated the need for strong group alignment. Communities form around a philosophical belief and consciously or not, we spend our time with those who we perceive as aligning our beliefs. In the case of bitcoin, the community formed around the belief in a concept known as “sound money.”

Bitcoin is Sound Money

The term “sound money” comes from a time when you could tell if a coin was made of a rare metal by listening to the sound it made when dropped on the table. If it was real silver, then you could hear it. Historically, sound money was considered the best kind of money (something that can be used as a unit of account, medium of exchange, and store of value. Sound money is limited in supply by necessity and acts as a check on the issuance of currency by a ruling party.

Last week, we spoke about how the world moved from sound money (gold-backed currency) to a world of free-floating currencies not tethered to any resource of limited supply. The transition gave rise to skepticism about the traditional system and its credibility, eventually leading to the creation of Bitcoin. Bitcoin took the concept of sound money and made it digital, embodying the traditional characteristics associated with those principles. Mainly...

Scarce - Limited supply of (Only 21 million will ever be created)

Divisible - Is highly divisible up to eight decimal places (You can hold 0.00000001 bitcoin)

Durable - Could not easily be destroyed. (You cannot destroy a bitcoin, BUT you can lose access to it)

Recognizable - People know your brand and trust it (BTC’s Orange “B” is becoming very well known.

Portable - Easy to move from one location to another. ($1B of BTC can easily be accessed as long as there is internet)

As with any project of passion, there were some within the bitcoin community who began to believe that this technology was not doing all it could do. Around 2010-- one year after the first bitcoin block was created, groups began to split off from the bitcoin community and start their own projects focused on what they believed bitcoin should be. Enter “alt coins.”

The Rise of Alt Coins (Alt Networks)

“Alt coin” is short for “alternative coin” and dates back to the early days in the digital asset space. Alt coins were referencing coins other than bitcoins and were originally a pejorative for projects that were not liked by the Bitcoin community. The first alt coin was created two years after bitcoin’s launch and was called Namecoin, but most of you are probably more familiar with one of the next alt coins launched: Litecoin.

Litecoin took the various innovations of bitcoin and made some slight tweaks. It wanted to be the silver to bitcoin’s gold. Litecoin aimed to accomplish this by reducing the time it would take to create a block (page in our Yap Island ledger) and increase the total supply of Litecoin (total number of Yap Island stones).

Put simply, the rest of the Bitcoin community was offended. In their eyes, the Litecoin community was violating the sound money characteristics laid out above. How could a currency be “sound money” if at any given time the community decides to increase the supply? And so the battle between bitcoin sound money hardliners and the rest of the blockchain community began.

An important nuance to this conversation is that up until 2016, every time a new digital asset was issued/created, it required a new blockchain. Going back to our Island of Yap, let’s say that a small group of Yapese wanted to make a change to the stone ledger system. This group believed that meeting twice a day to update their ledgers was better than once a day. The increase in frequency would mean that transactions in the morning would be recorded quickly, and the stones would be accessible to the recipients sooner.

Unfortunately the broader community did not have time to meet twice a day, and so they refused to change this rule. The smaller group would be forced to sail to a new island and create a new stone-based system that had the rules they wanted. Obviously the movement of the small community from Yap to an adjacent island would take a significant amount of effort.

The same was true in the blockchain space. The Litecoin community had to coordinate, set up infrastructure, and get other community members to connect to their new network. It was expensive and challenging. A young man within the Bitcoin community realized that there might be a way to create new digital assets without needing to create new networks. His name is Vitalik Buterin.

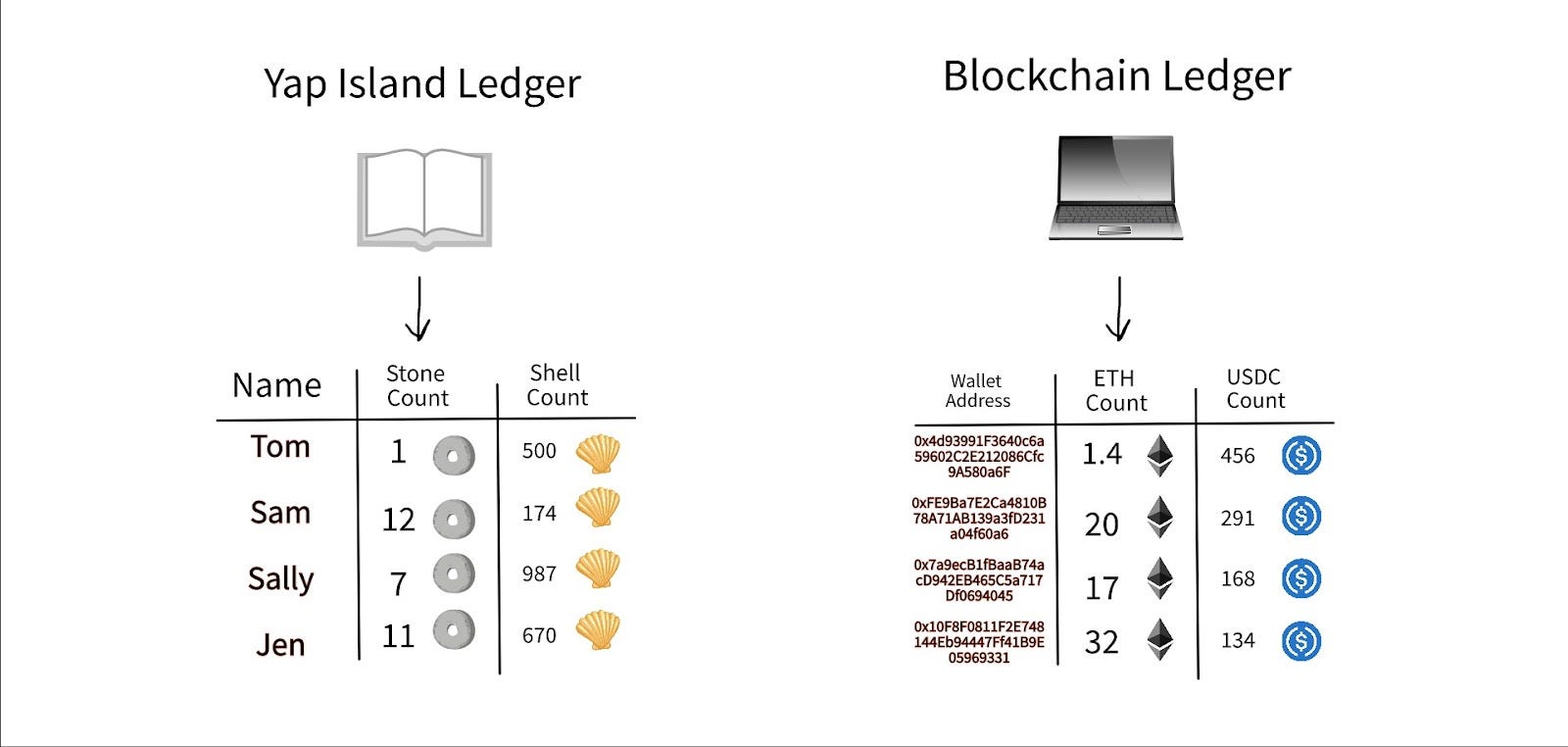

The Sea Shells

On the Island of Yap, the only object the Yapese would track was their stones. However, it's not hard to imagine a world where they also tracked the ownership of other valuable objects such as sea shells. Sea shells are more abundant on the island than stones are and can be used for smaller transactions. The ownership of sea shells would still be updated at the same rate that stones were, but they were used for smaller transactions. The idea of tracking other forms of value on a network is a core part of the second most popular network: Ethereum.

Ethereum was founded in 2016 by twenty one year old Vitalik Buterin and a team from the Bitcoin community. The group wanted to create a blockchain that would allow anyone to programmatically add new forms of value to their blockchain, thus reducing the need to create a new network every time a group wanted to create a new digital asset. Ethereum helped to transition from alt networks to alt coins. New forms of value began being created at an astonishing rate. Utility tokens, asset-backed tokens, and hybrid tokens that were once only imagined now became reality. Speculation about the potential implications of these new forms of value lead to the digital asset bubble of 2017.

Today, Ethereum is not the only network allowing other forms of value to be tracked on it. Competitors that have been alive for years such as Cosmos, Trezor, and Tron; and all attempt to improve Ethereum just like Litecoin tries to improve bitcoin. Even today, newer projects like Solana and Avalanche attempt to take the core principles of Ethereum and make them better. With these networks, we have moved into an age where blockchains no longer just underpin sound money but create a foundation for “sound value.”

Next week I will come back from this small tangent about the history of Blockchain and move back to a somewhat more technical discussion.